Personal Finance that Doesn't Suck

A basic guide to good personal finance.

Disclaimer: I am not a licensed financial advisor. This post is for educational and entertainment purposes only and reflects lessons I learned from my mistakes. It should not be construed as personalized investment advice. Research and consult a qualified professional before making any financial decisions. Past performance is no guarantee of future results.

Executive Summary:

Follow the 6-step process for financial freedom.

Step 0 before you start: budget and reduce your expenses, set realistic goals, and fix your money psychology.

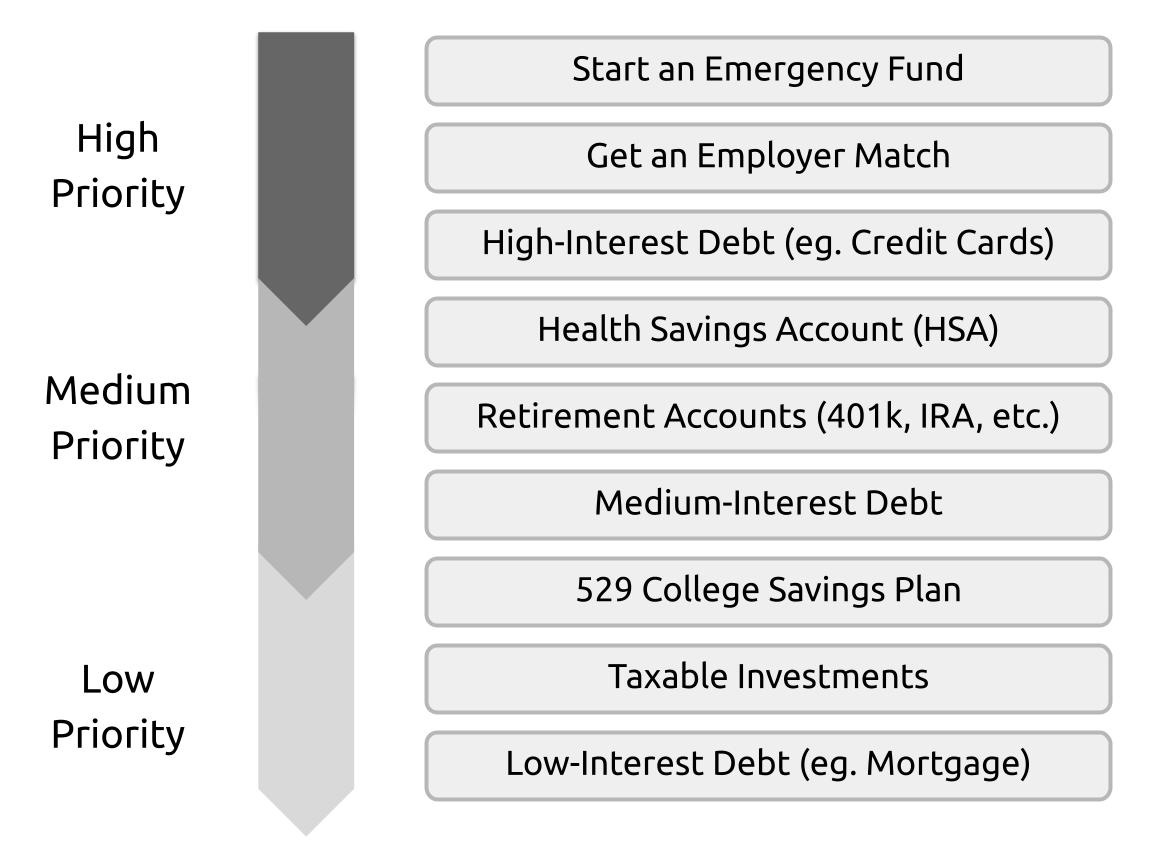

Build an emergency fund that covers 3-6 months of expenses.

Max out any employer-sponsored matching funds.

Pay down high-interest debts.

Open and contribute to retirement accounts. Start with an HSA if possible, then move on to accounts like the Roth/Traditional IRA and 401(k).

Save for everything else.

For investing:

Live below your means so you can invest early.

Keep your investments simple, diversified, and low-cost. Vanguard’s target retirement funds, VT, or VTI are all great options.

BUY AND HOLD AND DO NOT SELL.

Why read this post?

This post is a practical explanation and refresher on basic personal finance. I’m not a financial advisor; I'm a normal guy who wants to retire comfortably without selling my soul and grinding away my 20s, so I’m writing this post for myself too!

Accordingly, this guide is NOT about profit-maxxing; I won't help you get on that Sigma Male Gorillionaire Grindset. Instead, we’ll focus on risk-aversion and minimizing mental load, while still being able to live a good and financially stable life.

The goal is to retire with freedom and comfort, minimal effort, and as little risk as possible.

This guide is US-centric: government and employer programs will probably vary by country. At the very least, budgeting and money psychology are universal.

First, a list of sources of good information:

Humphrey Yang on YouTube

r/Bogleheads and the Bogleheads wiki

The Psychology of Money by Morgan Housel (you can probably find a PDF online somewhere, and there’s a great summary of the book on Reddit)

Investopedia (usually for technical details)

If you want to dive deeper into any of the topics I mention, go to those sources. And if I haven’t cited a piece of information, it’s probably somewhere in there. Hopefully, you won’t need to. For this post, I don’t care about originality: I only care about being right. If you catch something incorrect, please correct me in the comments!

A six-step guide to financial freedom

I won’t do any better than the r/personalfinance and Bogleheads wiki pages, so I won’t try. Instead, I’m going to synthesize their collective advice, summarize it in a short and readable form, and then go through each step one by one. Don’t worry if something doesn’t make sense yet—I’ll cover it in more detail later (you can also read the linked pages if you’re dying to know). Also, this list is not set in stone, so feel free to modify it to suit your personal needs or preferences.

From the Bogleheads wiki:

r/personalfinance also has an incredibly detailed visual flowchart that matches their wiki advice.

If at some point you find yourself stuck between two choices that both seem about equally good, flip a coin and pick one. It’s probably not that serious!

Remember: as long as you’re saving, you’re winning.

Step 0: Budget and reduce your expenses, set realistic goals, and fix your money psychology

Before you can start doing anything, you need to know how much you have, how much you spend, and how much you save. The r/personalfinance wiki has a list of tools for your perusal: I use Google Sheets’ monthly budget template, which I can edit on my phone. You can find it on Google Sheets, or make a copy of the template I just linked. Once you have, start tracking every expense or purchase you make. Once you have a good idea of how much you spend right now, you can start making targets for necessary expenditures like housing, food, and clothing. You can also portion out money for discretionary purchases like eating out, holidays, and luxury goods. Finally, and most importantly, you can decide on a good savings rate.

When tracking your expenses, be honest with yourself! This data will only help you make better decisions later on. You might realize that you’re paying for things you don’t care about, or that you’re being stingy on things that make a difference to you. Either way, you have to know. I found that I was eating out far more than I expected, that my other purchases were less expensive than I expected, and that my personal expenses mostly consisted of one-off purchases (as opposed to subscriptions or recurring services). Make sure to review your spending and savings habits throughout the month and at the end of the month. And prepare to be surprised!

Money psychology

You should really read The Psychology of Money by Morgan Housel. I am eternally grateful to my mom for making me read it in high school, and I will never be able to plug that book enough. Its fundamental insights are simple, but powerful:

Doing well with money has a little to do with how smart you are and a lot to do with how you behave.

The highest form of wealth is the ability to wake up every morning and say, “I can do whatever I want today.”

Figure out why you want money, set some goals, and be patient and aware of your behavior. Most people just want freedom, financial stability, and the ability to retire comfortably. And thankfully, becoming a financially responsible person is very simple! All you have to do is learn to avoid your weaknesses and blind spots, and make financially responsible decisions.

Unfortunately, simple does not mean easy. You’ll probably be revisiting Step 0 for the rest of your life. Focus on doing what’s reasonable over what’s optimal or perfectly rational. Remember, the point of money is to improve your quality of life and give you more freedom and stability. This idea will come back a few times in this post, as we consider tradeoffs that cost us money but bring us extra security.

Finally, different sources will give different recommendations on savings rates, often ranging from 10-20% of your income. In my opinion, it’s a better idea to make saving your default, instead of leaving spending as your default. Keep a minimum savings rate as a goal—but don’t aim to just barely achieve it, aim to surpass it! Saving money now will give you huge returns later on down the line, due to the magic of compounding. In general, if you’re spending less than you earn, you’re living below your means and doing a great job.

I’ll get into this more in the investing section.

Once you feel that you have some idea of what you’re saving for and what money means to you (or if you just want to move on now), proceed to Step 1:

Step 1: Build an emergency fund that covers 3-6 months of expenses

An emergency fund is essentially a piggy bank saved for emergency use. If you lose your income, get hit with an unexpected medical bill, or for whatever other reason need to draw upon your reserves, your emergency fund will be your cushion of funding that will save you from bankruptcy and allow you to bounce back. Your emergency fund should be liquid—you should be able to access it almost immediately—and it should always be full. A strong emergency fund will help you sleep better at night.

To be more precise, your emergency fund should have enough cash to cover 3-6 months of expenses. This is where Step 0 comes in handy! For example, I spend around $2,000 a month, so my emergency fund should be somewhere in the $6,000-$12,000 range before I move on to the next step. Whether you choose to keep 3 months, 6 months, or even more is dependent on your risk tolerance.

Choosing to keep a smaller emergency fund and invest the extra money might net you some extra gains over time, but it’ll leave you more vulnerable to unexpected life events—and those can happen at any time. I personally err on the higher end, trading away potential gains for some extra fiscal security, because it helps me sleep better at night. It’s your choice.

If you want to get fancy and make some money from your emergency fund, you can split it into tiers. For example, you might keep 1-2 months of expenses in a normal checking account with your local bank, and 3-4 months in something like a high-yield savings account (HYSA) or money-market fund. This might help you make some extra money, although the amount depends on the size of your emergency fund. For example, if you manage to place $4000 in a money-market fund with a 4% interest rate, you’ll make an extra $160 each year pre-tax.

I’m personally doing something like this—it makes me feel better about having a relatively large emergency fund. But this is super optional! If your eyes are glazing over at the thought, or trying to optimize your emergency fund is giving you anxiety, skip the tiering: just take the damn money and save it somewhere safe. Put it in a bank, put it in an HYSA, keep a stupid amount of cash in a safe or something. The most important thing is that you HAVE AN EMERGENCY FUND.

Once you have an emergency fund that can last you a few months, proceed to Step 2:

Step 2: Max out any employer-sponsored matching funds

Some companies will match your contributions to your 401(k).

A 401(k) is a U.S. employer-sponsored retirement savings plan—more on this later.

If your employer doesn’t match funds, or if you don’t have an employer-sponsored plan, skip to Step 3.

If your emergency fund is as full as you want it to be, you should max out this contribution match. This is literally free money: not taking it is like letting your employer keep some of your salary. For example, if you’re paid $40,000/year and your employer matches 401(k) contributions up to 3% of your salary, you can contribute $1,200 to your 401(k), and your employer will contribute the same amount. In other words, your employer just gave you a $1,200 raise!

Even better, that $1,200 gets to avoid some amount of taxes! For regular 401(k)s, your money is taken out of your paycheck before taxes are deducted—so you only have to pay taxes on it when you withdraw in retirement. Once the money is in your 401(k), you can start investing it. We’ll cover the details later: for now, just get that extra money from your employer.

Once you have, you can move on to Step 3:

Step 3: Pay down high-interest debts

If you have any high-interest debt (debt with an interest rate of 10-30%), you should start paying that down as soon as you’ve finished the first 2 steps. I suggest you choose one of two methods: you can pay your debt in order of the highest interest rate (avalanche), or pay the smallest debts first to build psychological momentum (snowball). Avalanche will save you more money in the long run, but if snowball makes you feel significantly better, you should go with that. Never forget: the purpose of money is to provide you with freedom and happiness! Don’t lose sight of what really matters.

If your loans have a minimum payment, you might consider paying the minimum each time. That’s not a terrible idea, but I personally think that the psychological benefit of being debt-free is unmatched. Either way, don’t stretch it out any longer than you have to. Also, consider using a site like unbury.me to help with planning.

Be very careful about taking on any extra debt. Never buy things if you can’t afford them from the get-go: paying in installments is a scam, and credit card debt is one of the worst and most predatory forms of debt out there. Having a credit card can give you extra benefits in the form of saving money with cashback and building your credit score, but ONLY IF YOU CAN PAY IT RELIABLY.

If you have a credit card, do not treat it as a source of extra money.

I have two credit cards—one with 1.5% cashback on all purchases, and one with 3% cashback on grocery stores, dining, and entertainment. These allow me to save a couple hundred extra dollars per year, and many other credit card options might allow you to do the same (e.g., Citi's Double Cash or Fidelity's Visa Signature). But I’ve automated my monthly payments so that I never have to pay interest, and I pay off my balances in full at least once a week.

If you don’t yet feel responsible enough to handle a credit card, or know you have tendencies towards impulse purchasing or even gambling, it might not be worth it for you. Only you will know what the right decision is.

Once you’ve either paid down your high-interest debts or decided on a smart and careful loan repayment strategy (imho preferably the former), proceed to Step 4:

Step 4: Open and contribute to retirement accounts

It’s time to invest in your future. The US has many different types of retirement savings accounts: Health Savings Accounts (HSAs), Traditional Individual Retirement Accounts (IRAs), Roth IRAs, 401(k)s, so on and so forth. The important thing is this: they all allow you to legally avoid some amount of taxes, as long as you’re saving for retirement. Legally avoiding taxes is like getting free money from the government!

If you withdraw money from these accounts before the age of 59 1/2, you’ll probably have to pay back-taxes + an early withdrawal penalty. There are some exceptions on Traditional and Roth IRAs that are out of scope for this article: for now, don’t touch your retirement savings unless your emergency fund has run dry and you have no other choice.

If you’re eligible to contribute to an HSA, do that first. If you’re not eligible or max it out, you can pick any of the other 3 and be fine. Personally, I’m not yet eligible for an HSA. I opened a Roth IRA with Fidelity because it was convenient and I heard good things about their customer service, and plan to open a 401(k) with my employer if possible. You could go with Vanguard instead—it’s not that serious.

If you’re planning to go to college or are dealing with college expenses right now, that might take priority over retirement savings. If so, consider returning to Step 1 and building out your emergency fund to a year of expenses, or maybe even longer if you think you might need it.

Remember, focus on your freedom and happiness. Don’t sweat the details too much: as long as you’re still saving, you’re still winning!

Step 5: Save for everything else

The Bogleheads wiki orders the rest as: paying off medium-interest debt, investing in a 529 college savings plan, investing in normal (taxable) investments just to have more savings, and paying off low-interest debt. You can absolutely follow those steps in order. If you have other ideas, do whatever floats your boat—I’m planning to open a normal investing account with Fidelity or Vanguard and start investing using the tips below.

But again, it’s not that serious. Once you’ve done steps 0-4, you’re in the clear!

A quick primer on investing

Before I can end this post, I need to cover how to invest your contributions.

Live below your means so you can invest early

EDIT: This section has been updated—thank you to my friend Allie for catching some mistakes I made in the first draft.

Exponential growth is really unintuitive, because compounding is magical. Here’s a retirement calculator with some basic details I filled in (you can adjust it to fit your life circumstances).

As you can see, if I can make a pretty reasonable 7% yearly return on my investments in the market, saving even $1000/month and increasing my savings contribution by 3% every year is enough to get me to $5,292,271 by the time I retire. After 45 years of career progression, my monthly contribution would need to be $3,781.56 (or $45,378.72 annual). This seems very doable. And I still end up with $522,261 after I die at age 90!

Personally, I’m paranoid about future life expenses, medical emergencies, and the plethora of other possible events that might force me to dip into my savings or stop contributing to retirement, so my goal is to save even more if possible. I will report back with more detail once I get my first full-time job (still working on converting my internship to a full-time position), but assuming yearly expenses of $25,000 ($2,083.33 monthly) and a starting income of $40,000 after-tax ($20/hour after tax), my yearly savings would be $15,000 ($1,250 monthly). That’s $250 per month ($3,000 yearly) for unexpected expenses, or that much more of being ahead!1

To invest these amounts into my retirement funds, I’m going to have to live below my means—living with roommates in cheaper neighborhoods, eating out as little as possible, tracking all my personal expenses, using public transport instead of buying a car (I’m lucky to live in Chicago), etc. etc. I’m a little skeptical about these calculators, because many seem to give vaguely different results, which is why I’m saving more than strictly necessary. Either way, the point remains: save money and invest early!

Remember: time in the market beats timing the market.

Keep your investments simple, diversified, and low-cost

When investing in stocks, don’t try to beat the market. Over long periods, the US economy and global economy tends to expand—and the market as a whole tends to rise with it. However, you’re not going to have the knowledge to pick out the individual funds that will rise more than the others—that’s just gambling, and is a TERRIBLE idea. If you’re wrong, you’ll lose money. Even worse, if you’re right, you’ll get a taste for gambling in the stock market, which might be even worse for you in the long-run.

By investing in a low-cost index fund like VTI, Vanguard’s Total Stock Market Index Fund ETF, you can essentially avoid the risk associated with any particular fund, and instead invest in the entire US stock market—meaning that your only risk is the entire US economy collapsing. And by investing in an index fund like VT, Vanguard’s Total World Stock Index Fund ETF, you can invest in the whole world! Even the best financial advisors struggle to outperform well-managed index funds.

If you want even more financial stability, consider investing in government bonds. Bonds give smaller returns but have less volatility involved; stocks tend to do better over periods measured in decades, but if you're close to retiring or simply want stability, bonds can bring you some real peace of mind. If you don't want to think about it, target retirement funds like Vanguard's or Fidelity’s will slowly switch your investments from stocks to bonds automatically over time, reducing your volatility as you get closer to retirement.

But don’t sweat the details too much! I’m personally split between VT, VTI, and Fidelity’s target retirement funds, but that's just based on vibes. The precise decisions you’re making aren’t nearly as important as the fact that you’re making them.

Remember: time in the market beats timing the market.

BUY AND HOLD AND DO NOT SELL

Markets are volatile in the short term but historically have gone up in the long term. If you’re invested in an index fund that covers the whole market, the worst thing you can do in a market crash is sell. As long as you hold on to your positions and don’t do anything reckless, you’ll eventually recoup your losses. If you sell, you lock in your decision and turn your potential losses into actual losses.

Holding in a crisis might sound easy. It is anything but.

If, like me, you’re too young to remember the 2008 financial crisis and you want to see what it’s like when things go REALLY wrong, check out this r/bogleheads thread about the 2008 financial crisis and the linked thread on the Bogleheads forum during the crisis itself. Holding during a crash like that requires an insane amount of discipline, faith in your plan, and mental fortitude. Imagine checking your retirement accounts in 2008 and finding that you’d lost HALF of your retirement savings. Even worse, imagine having to wait three full years until you regain what you’d lost.

But if you never sold, and held on to VTI for the past 17 years, you’d never know the difference: your money would have tripled in value, and you’d still be right on track for retirement. The more decisions you make, the higher your chance of messing something up. So don’t just do something, stand there! And maybe even forget your password (don’t actually do this one, but the point still stands).

This is another good reason to hang on to bonds, which aren’t subject to the same kind of volatility. I used to discount them as an investment tool, since I was after those sweet stock market gains, but then I lost 15% of my retirement portfolio essentially overnight during Trump’s liberation day tariff shenanigans. Even with my tiny retirement savings portfolio built up during college, I still got cold feet and rebalanced from the US-centric VTI to the global VT. I now have a much greater respect for the psychological distress that market crashes can bring.

Remember: time in the market beats timing the market.

And that’s the game!

Over the next few weeks, I plan to go through this information in more detail and cover topics that I wish I’d known about before I started investing. I’ll be writing more articles on the psychology of money, along with a more detailed exploration into the world of investing for retirement.

But if you’re sick of all this financial-literacy-posting, don’t sweat it. You are now armed with all the knowledge you need to live a decent life and retire comfortably. Unless the world ends tomorrow—but if that happens, you’ll have bigger things to worry about.

Now go forth and be financially responsible!

Believe it or not, these numbers are still moderately conservative. My actual monthly expenditures are probably closer to $24,000/year ($2,000/month), and my actual post-tax take-home income will probably be closer to $43,000/year, leaving me $19,000/year of savings ($1,583.33/month). That being said, I generally leave a lot of room for leeway—see my post on money psychology for more details.

in knowing you well for 6? 7? years now i just wanted to say you have a gift of making knowledge i find unapproachable feel more approachable!! personal finance scares me less now. thanks for existing and writing!!